The RBI and its Growing Fiscal Role

Central banks in modern democracies occupy a peculiar position. While governments spend, tax, and borrow to meet political mandates, central banks manage inflation, preserve confidence in the currency, and safeguard financial stability. Their credibility hinges on maintaining a degree of institutional distance from the immediate fiscal compulsions of the governments they serve.

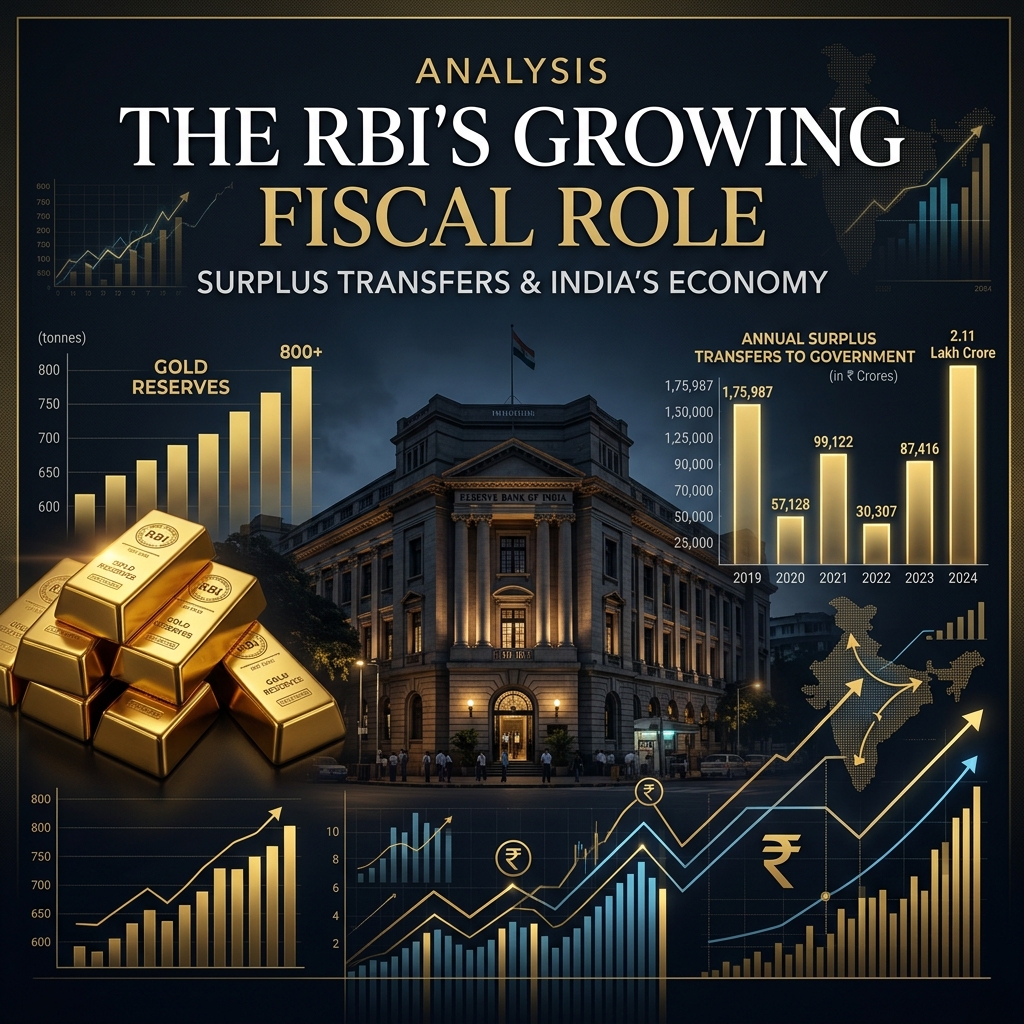

However, recent developments surrounding the Reserve Bank of India (RBI) highlight a progressive shift in this relationship. In May 2026, the RBI approved a record surplus transfer of ₹2.87 lakh crore to the Union government for the fiscal year FY26. While fully consistent with the established Economic Capital Framework, the scale of this transfer raises significant questions about the evolving role of the central bank within India's broader fiscal architecture.

I. A Structural Shift: The Scale of the Surplus

Historically, RBI surplus transfers to the Central Government hovered around the ₹30,000 crore to ₹65,000 crore range. The tipping point occurred in 2019 following the implementation of the revised Economic Capital Framework (ECF) recommended by the Bimal Jalan Committee. Under this framework, excess contingency buffers are systematically released to the sovereign once the risk buffers cross the mandated thresholds.

This year's record-high transfer of ₹2.87 lakh crore is a major leap, coinciding with a phenomenal growth of the RBI's balance sheet. The RBI's balance sheet increased by 20.6% in a single year to ₹91.97 lakh crore by March 2026, while its gross income rose by over 26% during the same period. This scale means the surplus transfer alone is now larger than the annual budgets of several Indian States.

II. The Mechanics: Where Do the Earnings Come From?

Central bank profits do not mirror standard commercial earnings. The RBI's surplus represents a return on its massive portfolio of domestic and foreign assets, interest earned on government securities, and foreign exchange interventions. Because the RBI acts to manage the exchange rate and stabilize rupee pressures, its market operations often yield substantial gains.

According to recent reports, the RBI sold approximately $12 billion worth of gold and purchased foreign-currency assets of about $7.5 billion to address rupee exchange rate volatility. The resulting portfolio adjustments, along with high yields on foreign currency reserves and interest earned on securities holdings, generated the massive gross income that made this record-high dividend possible.

III. The Federal Blind Spot

Perhaps the most contentious aspect of this fiscal evolution is its impact on cooperative federalism. Under the Indian Constitution, the divisible pool of tax revenues (such as corporate tax, personal income tax, and GST) is shared between the Center and the States based on formulas determined by the Finance Commission.

However, the RBI's surplus transfer is classified as non-tax revenue. Because it is non-tax revenue, it belongs exclusively to the Union Government. There is no mechanism for automatic devolution of these transfers to the States. This exclusion exacerbates a growing structural imbalance:

- High State Obligations: State governments bear the primary burden of developmental, social welfare, and infrastructural spending on the ground.

- Borrowing Caps (Article 293): States face strict limits on their borrowing capacity under Article 293, leaving them with very little fiscal flexibility.

- Centralized Revenue: The rise of non-divisible revenues, such as central cesses, surcharges, and direct dividend transfers, effectively shifts the fiscal landscape of India towards the Centre.

IV. Guardian of Stability or Fiscal Instrument?

The debate over the surplus transfer is ultimately not just about the money itself; it is about the changing role of the central bank within the sovereign economy. The RBI has evolved from being primarily a guardian of monetary and price stability into an increasingly important pillar of national fiscal capacity.

The Balance Sheet Debate: Two Perspectives

1. The Fiscal Support View: The surplus transfer eases borrowing pressures for the Central Government, helping manage the fiscal deficit without crowding out private investments. In times of global macro headwinds, it provides crucial non-inflationary resource mobilization.

2. The Independence View: Accumulating excessive reliance on central bank dividends can lead to a 'fiscalization' of monetary policy. If the RBI's asset allocation and foreign exchange transactions are driven even partially by the target dividend size, it could dilute the central bank's focus on price stability and emergency buffer preservation.

To be clear, the RBI continues to operate within a well-defined framework and retains substantial operational autonomy. Its contingency buffers have been maintained at safe ECF-mandated limits. Yet, as surplus transfers become a larger, recurring feature of the Union's budget math, preserving the institutional distance between the central bank and the sovereign's fiscal needs will require deliberate, transparent governance.

V. Conclusion

As India navigates its path towards sustainable high growth, the coordination between monetary and fiscal authorities is more critical than ever. The RBI’s record surplus transfer has given the government vital breathing space. However, for long-term fiscal health, India must look beyond one-off non-tax windfalls, address the borrowing challenges of States, and continue guarding the autonomy of its most vital monetary institution.

Study Smarter on GyanGram

Swipeable flashcards. PYQ-mapped topics. Built for UPSC Prelims.