Is the RSS a Legal Person? Decoding Voluntary Associations & Indian Law

Syllabus Connection: GS Paper II

GS Paper 2: Polity & Governance — Non-governmental organizations (NGOs), voluntary associations, self-help groups, regulatory bodies, and compliance/financial transparency rules.

💡 Key Takeaways for UPSC Prep

• Legal Personhood: Natural persons are living human beings, while juridical/artificial persons (companies, registered societies) are entities created by law possessing independent rights and liabilities.

• Unregistered Status: As an unregistered body of individuals, the RSS lacks juridical personhood and is not a corporate body, but operates under mutual association principles.

• Mutual Tax Exemption: High Court rulings in the 1970s exempted the RSS's member donations (Gurudakshina) from income tax, applying the legal principle of mutuality (an association cannot profit from its own members).

• Suits & CPC Representation: While unregistered bodies generally cannot sue or be sued, the Supreme Court in Singhai Lal Chand Jain v. RSS (1996) ruled that a suit is valid if representatives (e.g. managers/presidents) defend it jointly.

• The FCRA Barrier: Under the Foreign Contribution (Regulation) Act, 2010, an association must be registered under a statute (such as a Society, Trust, or Section 8 Company) to accept foreign donations, legally barring unregistered bodies.

Natural vs. Juridical Personhood: How Indian Law Classifies Legal Entities

In jurisprudence, the concept of "personhood" is central to determining rights and obligations. According to legendary legal theorist John Salmond, "A person is any being whom the law regards as capable of rights and bound by legal duties." Under Indian law, persons are divided into two distinct categories: **natural persons** (living human beings) and **juridical or artificial persons** (entities created by law that hold legal rights separate from the individuals who compose them).

Juridical personhood is typically acquired through statutory registration. For example, a company registered under Section 9 of the Companies Act, 2013 becomes a body corporate with perpetual succession, a common seal, and the capacity to own property, contract, and "sue and be sued" in its own corporate name. Similarly, registered cooperative societies and deities in temples are recognized as juridical persons. Unincorporated entities, such as unregistered clubs or voluntary associations, do not possess this independent legal identity, meaning the law treats them as a collection of individuals rather than a single entity.

The Legal Character of the RSS: An Unincorporated Body of Individuals

The Rashtriya Swayamsevak Sangh (RSS) has repeatedly described its own organizational structure as a voluntary socio-cultural organization and a "body of individuals." The organization has no formal membership registers, no application forms, no membership fees, and no written constitution-mandated rolls for day-to-day members—anyone can join simply by attending a local *Shakha* (daily assembly). This lack of statutory incorporation means that the RSS does not possess independent juridical personhood under civil law.

However, public law recognizes unregistered bodies for regulatory purposes. Under Section 2(31) of the Income Tax Act, 1961, the definition of a "person" is defined expansively to include a **"body of individuals (BOI), whether incorporated or not"** and an **"association of persons"** (AOP). In cases such as Commissioner of Income Tax v. Rashtriya Swayamsevak Sangh (1994), the courts recognized the RSS as an unincorporated association for tax filing and assessment, showing that statutory laws can create specific legal identities for unregistered groups even if they lack general corporate personhood.

The Taxation of Gurudakshina: The Principle of Mutuality in Action

Because the RSS charges no membership fees, its operations are funded entirely by voluntary contributions from its volunteers. These contributions are made annually during a ceremony known as *Vyasa Puja*, where members offer *Gurudakshina* (a traditional token of gratitude to the teacher, represented in the RSS by the saffron flag or *Bhagwa Dhwaj*). During the 1970s, the tax status of these donations came under intense judicial scrutiny during assessment proceedings in Bombay, Patna, and Nagpur.

The Income Tax Department argued that *Gurudakshina* received from volunteers constituted taxable income. However, the Patna High Court and other appellate tribunals held that the funds were voluntary offerings given out of reverence, qualifying as tax-exempt. More importantly, the rulings applied the **principle of mutuality**—a foundational tax concept holding that where a group of people contribute to a common fund for their mutual benefit, any surplus returned or held does not constitute "profit" or taxable income, because "no one can make a profit out of themselves." This principle protects voluntary mutual associations from being taxed on internal contributions.

Can an Unregistered Body Sue or Be Sued? The Singhai Lal Chand Jain Precedent

As a general rule in civil procedure, an unregistered body cannot sue or be sued in its own name. Because it is not a legal person, it cannot hold property directly or enter into contracts in its collective name; any transactions must occur through its individual members or trustees. If a dispute arises, this lack of legal personhood presents a significant hurdle for litigants seeking civil remedies against the group.

To prevent unregistered organizations from escaping legal liabilities, the Code of Civil Procedure (CPC) provides a mechanism under **Order 1 Rule 8** for **representative suits**. This rule allows a lawsuit to be filed against a few individuals representing the entire unincorporated body. The effectiveness of this rule was tested in the Supreme Court case Singhai Lal Chand Jain v. Rashtriya Swayamsevak Sangh (1996). The case involved a landlord seeking to evict the RSS from rented premises in Panna, Madhya Pradesh. The tenant argued that the eviction decree was invalid because the RSS was an unregistered body that could not be sued. The Supreme Court rejected this defense, ruling that since the RSS was represented in court by its manager, president, and members who jointly and actively defended the suit, the eviction decree was valid and binding on the entire body.

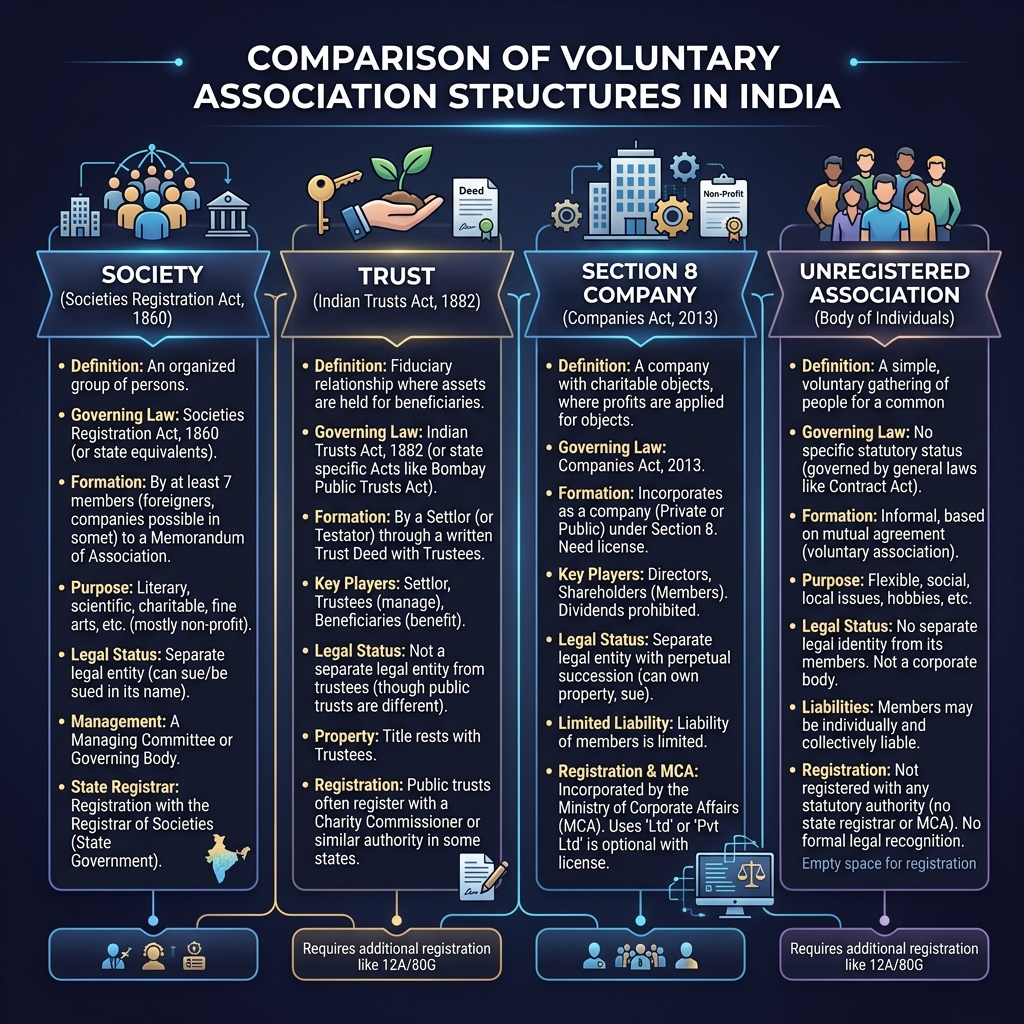

The Regulatory Matrix of Voluntary Associations and the FCRA Barrier

For citizens and organizations seeking to establish a voluntary or non-governmental organization (NGO) in India, the legal framework offers three main statutory structures. Unincorporated associations like the RSS choose to remain outside these structures, which eliminates statutory reporting requirements but imposes significant regulatory barriers, particularly regarding foreign funding.

Under the **Foreign Contribution (Regulation) Act (FCRA), 2010**, no association or NGO can accept foreign donations or hospitality unless it obtains registration or prior permission from the Ministry of Home Affairs. To qualify for FCRA registration, the law mandates that the applicant must be registered under an existing statute (such as the Societies Registration Act, 1860, the Indian Trusts Act, 1882, or Section 8 of the Companies Act, 2013) and must have been active for at least three years. Consequently, unincorporated bodies like the RSS are legally barred from accepting any foreign contributions, representing a strict regulatory check on unregistered organizations.

| Structure | Governing Act | Juridical Personhood | FCRA Eligibility | Suits (Sue/Be Sued) |

|---|---|---|---|---|

| Society | Societies Registration Act, 1860 | Limited Juridical Personhood | Yes (After 3 years of activity) | In name of President/Secretary |

| Trust | Indian Trusts Act, 1882 | No (Vests in Trustees) | Yes (After 3 years of activity) | Through Trustees |

| Section 8 Company | Companies Act, 2013 | Full Juridical Personhood | Yes (After 3 years of activity) | In corporate name directly |

| Unregistered Body (e.g. RSS) | None (Body of Individuals) | No Juridical Personhood | No (Statutorily Barred) | Only via representative suits (CPC O1 R8) |

Finally, this unregistered status creates a unique legal arrangement with RSS-affiliated organizations (the Sangh Parivar). While the parent RSS body operates as an unregistered association, its 32+ sister organizations—such as the student wing Akhil Bharatiya Vidyarthi Parishad (ABVP, registered July 9, 1949, under the Societies Registration Act), the trade union Bharatiya Mazdoor Sangh (BMS), and its educational wings—are registered legal entities. This allows the affiliates to navigate statutory requirements, open bank accounts, own corporate properties, and apply for tax benefits or FCRA approvals, while the parent body maintains its character as a voluntary, unincorporated assembly of individuals.

Frequently Asked Questions

Is the RSS a registered legal person under Indian law?

What is the tax status of Gurudakshina received by the RSS?

Can an organization like the RSS sue or be sued?

Can the RSS receive foreign funding under FCRA?

Are RSS-affiliated organizations registered?

GyanGram Editorial Note

This analysis is based on the explainer "Is RSS a legal person?" by Rizmi Lia M., supplemented by statutory provisions under the Income Tax Act, 1961, Companies Act, 2013, Civil Procedure Code, 1908, and the FCRA, 2010. Formatted for UPSC GS Paper II (Polity & Governance) preparation.